The FTC’s March 2026 warning letters to 97 auto dealership groups marked a turning point: the agency is enforcing total-price disclosure case by case, and OEMs in powersports, marine, RV and LSV are already advising dealers to revisit how they advertise. This piece breaks down where dealers actually get exposed, why the same patterns extend across every titled-vehicle segment, and how disclosure-by-design turns compliance into a byproduct of a cleaner buyer experience.

A familiar problem, now getting prosecuted

On March 13, 2026, the Federal Trade Commission sent warning letters to 97 auto dealership groups across the country. The message, in plain terms: the price you advertise must be the total price a consumer is required to pay — including every mandatory fee. The agency cited a tight list of practices it considers illegal under Section 5 of the FTC Act, among them advertising prices that exclude required fees, advertising prices that depend on the buyer using dealer financing, requiring add-ons that aren’t disclosed up front, and advertising vehicles that aren’t actually available.

It was not an isolated salvo. In November 2025 the FTC moved against Asbury Automotive Group for charging customers for add-ons they hadn’t agreed to or were told were mandatory. That case settled in March 2026, with full refunds and additional penalties on top. Earlier in the cycle, similar actions landed against Lindsay Chevrolet and Leader Automotive Group. The agency’s pattern is becoming legible: warn the field, settle the cases, set the precedent.

What dealers and counsel have seen this year is not a new rule — it’s a new tempo. The FTC’s CARS Rule, the dedicated motor-vehicle dealer rulemaking finalized in late 2023, was vacated by the Fifth Circuit on January 27, 2025, on procedural grounds. But the underlying authority the FTC uses to police deceptive pricing didn’t go anywhere. Section 5 of the FTC Act still prohibits unfair and deceptive acts. State mini-FTC acts and consumer-protection statutes still apply. And the agency’s broader Rule on Unfair or Deceptive Fees — 16 CFR Part 464, effective May 5, 2025 — sets out the disclosure principles the Commission now signals it expects to see across regulated commerce.

The takeaway for dealers is simple. Whatever you thought CARS was going to require, the FTC now plans to get there a different way: case by case, letter by letter, and in coordination with state attorneys general.

Why this hits powersports, marine, RV and LSV next

The most under-appreciated signal of the past month wasn’t the FTC’s letter — it was the OEM response. After the warnings landed, Ekho got word from dealer partners that multiple major non-car (powersports, LSV, etc.) vehicle manufacturers circulated guidance to their U.S. dealer network advising them to revisit advertising and pricing practices and to consult counsel. The framing was unmistakable: the FTC’s auto enforcement is being read as portable. If your dealership advertises a price that doesn’t include doc fees, freight, prep, dealer-installed accessories, mandatory add-ons or financing-contingent discounts, the analysis is the same whether you sell sedans, side-by-sides, pontoon boats, motorhomes or low-speed vehicles.

Powersports and other titled-vehicle segments share the structural exposures the FTC has spent two years documenting. Advertised prices that aren’t out-the-door prices. Doc fees that surface at signing. Freight and assembly that appear after the buyer has already invested time and emotion in the deal. Required accessories that weren’t in the listing. Financing-conditioned promotions where the cash buyer pays more. None of those practices are illegal because of the vehicle type. They’re potentially illegal because of how the price is communicated.

The OEM caution circulating now is best read as a leading indicator. The agency is busy with auto. The disclosure principles it’s enforcing are segment-agnostic — applying to all types of motor vehicles.

Where dealers actually get exposed

The exposure isn’t usually in headline pricing. It’s in the gap between the advertised number and the contract.

A handful of patterns recur in nearly every recent enforcement matter:

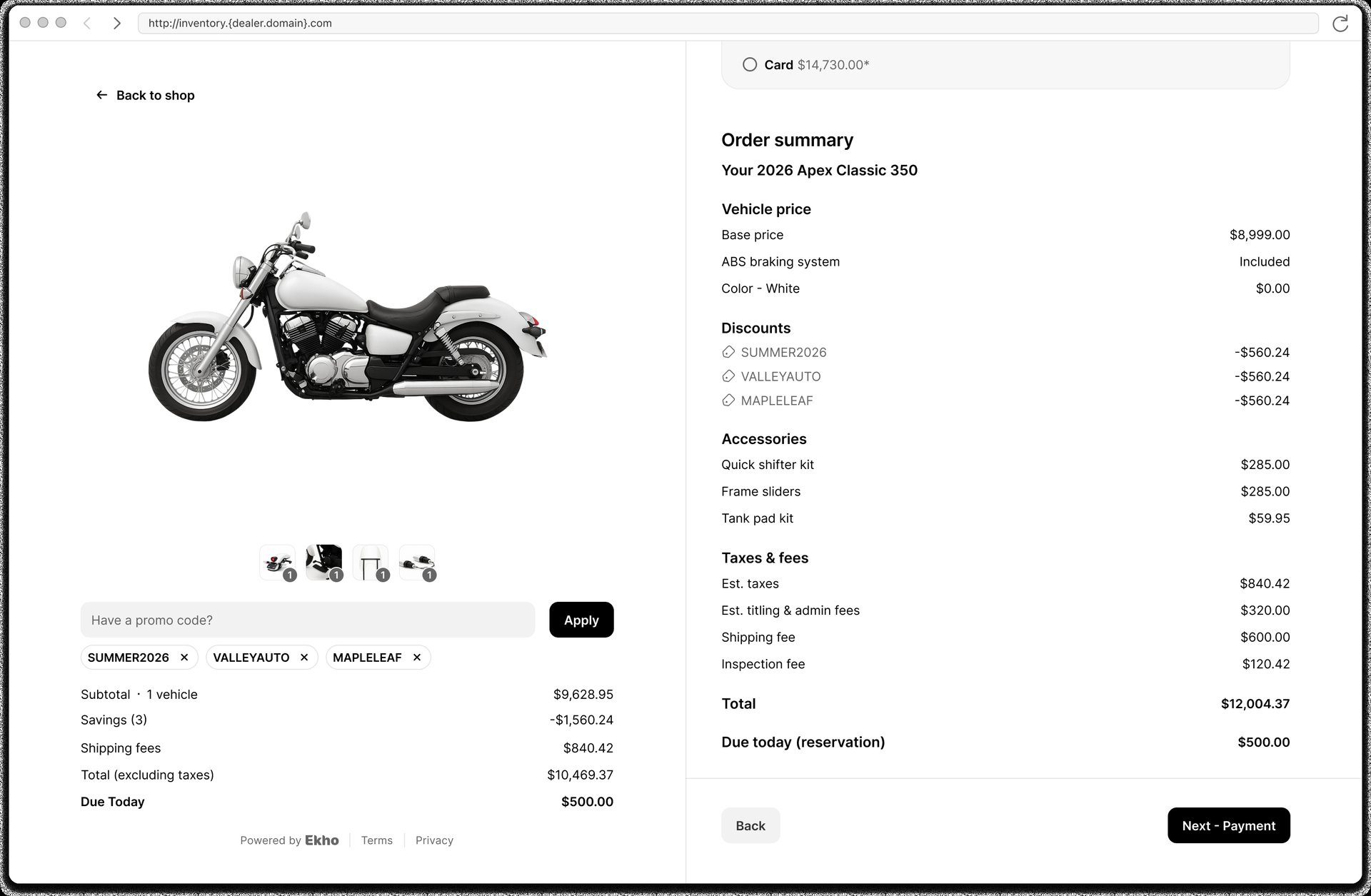

- The advertised price isn’t the total price. Mandatory dealer fees, required documentation fees, mandatory add-ons, required market adjustments — anything a buyer cannot decline and still walk out with the vehicle — belongs in the advertised total.

- Discounts that aren’t really available. Promotions that depend on stacking incompatible rebates, conditioning a price on financing through the dealer, or requiring trade-ins the buyer doesn’t have create a price the average shopper can’t actually get.

- Add-ons revealed at the F&I desk. Theft-deterrent etch packages, paint and fabric protection, GAP, service contracts and similar products are not inherently problematic — but presenting them as required, pre-checked or already priced into the deal is.

- Doc-fee surprise. A line item that appears for the first time on the buyer’s order is a textbook hidden-fee fact pattern, regardless of state-by-state caps.

- Inventory bait. Advertising a vehicle that isn’t physically available, or that requires additional fees the listing didn’t disclose, is one of the practices the FTC’s March letters call out by name.

What makes these patterns hard to fix isn’t the rule — it’s the workflow. Most of these moments live in the seam between advertising systems, DMS, F&I menus and finance applications. The customer experiences a single transaction; the dealership executes it across four or five tools that don’t agree on what the deal looks like.

The agency isn’t asking dealers to give up margin. It’s asking them to communicate the deal a buyer is actually going to sign.

Compliance as a byproduct of better UX

There’s a quieter framing that gets lost in the legal-update churn: every practice the FTC is targeting is a practice that erodes buyer trust. Buyers don’t enjoy out-the-door surprises. They don’t enjoy discovering the advertised price required a financing contingency they didn’t want. They don’t enjoy add-ons that show up on the contract without a clear conversation. The cohort of vehicle buyers who would prefer transparent, itemized pricing has been growing for years across every titled-vehicle segment, and a meaningful share of them are now comfortable transacting fully online when the experience is honest.

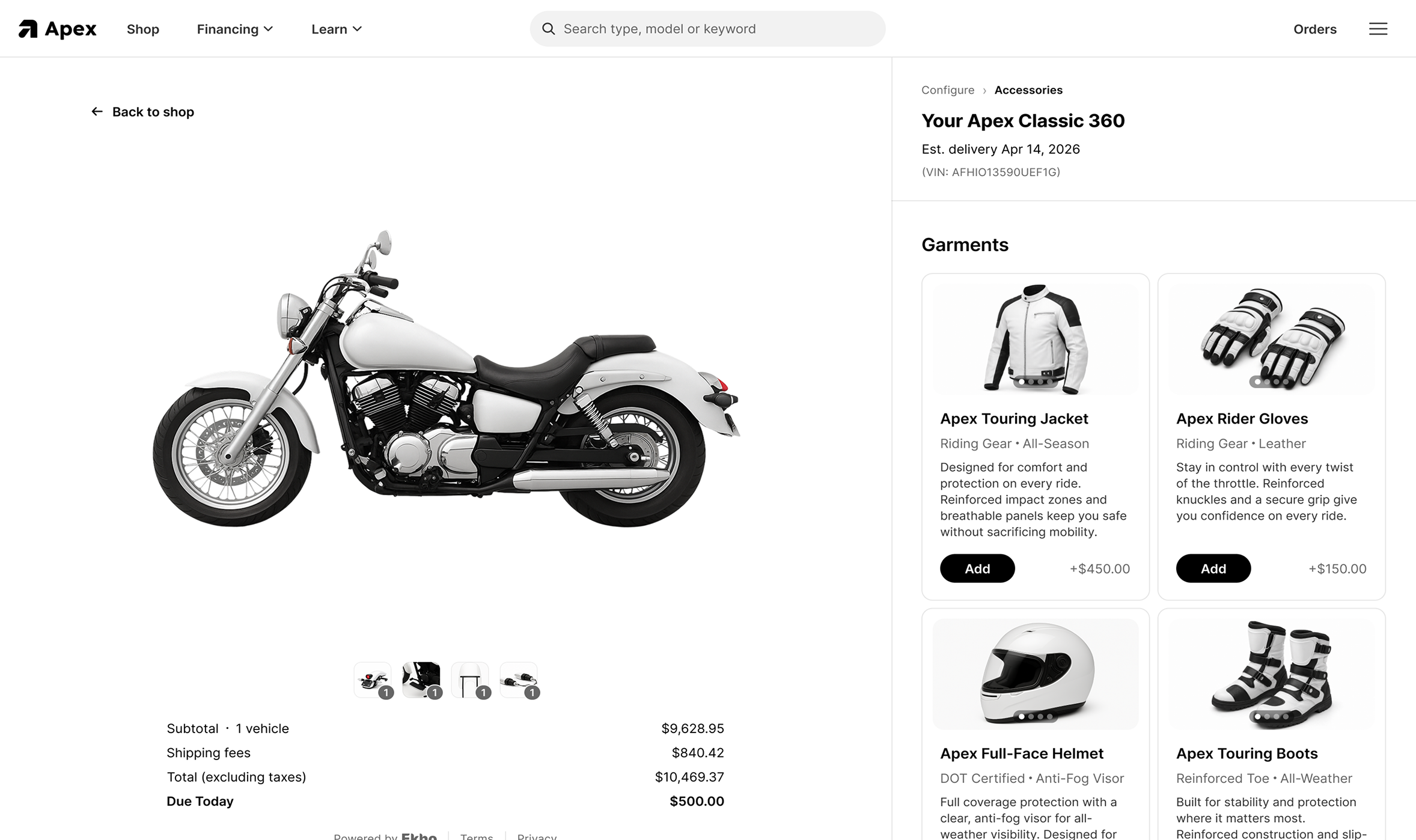

That alignment is the opportunity. When the entire transaction — vehicle price, mandatory fees, taxes, government charges, optional accessories, F&I products, financing terms — is itemized in a single flow that the buyer reviews before they sign, the FTC’s disclosure expectations are largely satisfied as a structural property of the system, not a checklist bolted onto a fragmented process. The total price is the total price, because the system has no other number to display. Optional add-ons are optional, because the buyer chose them on a screen with their cost next to them. Financing-conditioned offers are visible as such, because the math is transparent.

This is what AI-native, end-to-end vehicle commerce looks like when it’s built properly. Compliance is the byproduct, not the goal. The goal is a clean transaction the dealer can defend and the buyer trusts.

The same disclosure principles extend upstream of checkout. Ekho's AI Sales Agent is designed to be aligned with the FTC's guidance on motor vehicle pricing — breaking out vehicle price, mandatory fees, taxes, optional add-ons and financing terms in the pre-purchase conversation, so a buyer arrives at the dealership already understanding what they're going to pay. The result is fewer awkward reconciliations in F&I and fewer surprises at the desk. Dealers retain full control over how the agent talks about pricing — the guardrails, language and disclosure framing are configurable. The transaction engine handles disclosure at checkout; the Sales Agent handles it in the conversation that gets a buyer there. Together they cover the buyer journey end-to-end.

What dealers should do now

The path forward doesn’t require a rebuild — but it does require a real audit. A practical short list for the next 30 days:

- Audit advertised prices against actual out-the-door prices. If the gap is non-trivial, the advertised price needs to change, or the fees folded in need to come out of the deal.

- Map every required add-on. If something is universally installed and charged, it’s part of the price. If it’s optional, it must look optional in the workflow.

- Inspect F&I menu presentation. Pre-checked, pre-priced or implicitly required products are the highest-risk surface in most stores.

- Reconcile advertising claims with available inventory. A unit advertised must be a unit a buyer can actually purchase under the advertised terms.

- Document disclosures end-to-end. A buyer who understands the deal before they sign is a buyer who is unlikely to file a complaint and a dealership that can defend its practices to a regulator.

Dealers who treat the FTC’s pivot as a competitive opening — not a compliance burden — will end up with cleaner stores, better online conversion, and a structural advantage as enforcement spreads from auto into every titled-vehicle segment. The buyers were already asking for this. The regulator just made it urgent.

Learn how Ekho’s transaction engine itemizes price, fees, add-ons and financing in a single buyer-facing flow — and why disclosure-by-design is built into the architecture.

Frequently asked questions

In March 2026, the FTC sent warning letters to 97 auto dealership groups stating that the advertised price must be the total price a consumer is required to pay, including all mandatory fees. The agency has also pursued enforcement actions and settlements against dealers for deceptive pricing practices, signaling a new tempo of case-by-case prosecution.

Yes. The FTC’s disclosure principles are segment-agnostic and apply to all titled vehicles. After the auto warning letters landed, multiple major non-auto vehicle manufacturers circulated guidance to their dealer networks advising them to revisit advertising and pricing practices. The same legal analysis applies whether you sell sedans, side-by-sides, boats, or motorhomes.

The FTC targets practices like advertising prices that exclude mandatory fees, conditioning discounts on dealer financing, presenting add-ons as required when they are optional, surprising buyers with doc fees at signing, and advertising vehicles that are not actually available under the advertised terms.

The FTC is not asking dealers to give up margin -- it is asking them to communicate the deal the buyer is actually going to sign. When the entire transaction is itemized in a single flow that the buyer reviews before signing, disclosure expectations are satisfied as a structural property of the system rather than a checklist bolted onto a fragmented process.

Dealers should audit advertised prices against actual out-the-door prices, map every required add-on to determine if it belongs in the advertised price, inspect F&I menu presentation for pre-checked or implicitly required products, reconcile advertising claims with available inventory, and document disclosures end-to-end across the buyer journey.

Dealers who treat disclosure requirements as a competitive opening rather than a compliance burden end up with cleaner stores, better online conversion, and a structural advantage as enforcement expands. Buyers have been asking for transparent, itemized pricing for years, and the regulatory shift makes adopting it urgent.