Most digital-retail tools — and marketplace “Buy Now” buttons — quietly hand the deal back to the dealer’s back office the moment anything real has to happen. This piece walks through the six places online vehicle sales actually break (financing, stipulations, F&I, tax, titling, signing) in the order they show up in a deal, what each one costs the dealer, and what real checkout-to-keys infrastructure has to absorb instead.

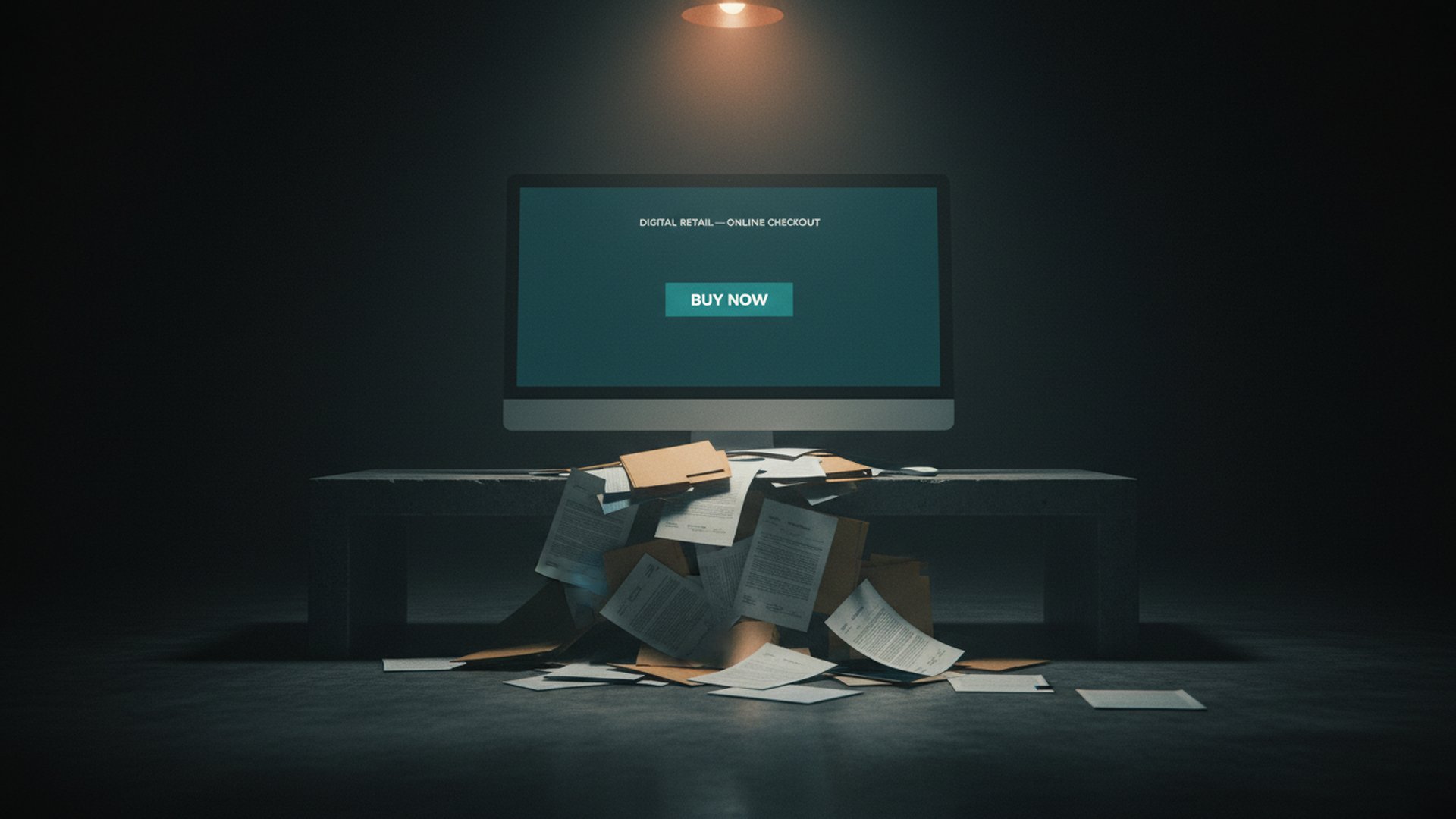

You’re paying for “online checkout.” You’re getting a lead form in costume.

You’ve seen it on the marketplaces. A bright button on every listing that says Buy Now. The buyer clicks. Their info drops into your CRM. Then — surprise — your salesperson calls them, your F&I manager rebuilds the deal at the desk, and your title clerk runs the paperwork the same way they did in 2010.

That’s not online vehicle sales. That’s a lead capture form with a checkout-themed costume.

Most digital-retail tools are wearing the same costume. The buyer self-serves the parts that don’t matter — picking a vehicle, running a payment estimator, dropping a deposit — and then the deal hand-offs to a human inside your store the moment anything real has to happen. Financing. Tax. Titling. F&I. Signing a contract a lender will actually fund.

If you’re paying for “online checkout” and your back office is still doing 100% of the work between yes and delivered, you’re not selling online. You’re generating leads with extra steps.

Six places your “online deal” quietly breaks

Each one is a deal you almost closed, an aftermarket dollar you almost earned, or an hour of back-office labor you can’t bill for. They show up in this order in a real deal.

1. Your checkout is quoting payments your lenders won’t fund

Your buyer enters their info. Your tool spits out a payment number. The buyer commits emotionally to that number. They imagine the unit in their driveway. They tell their spouse what it’ll cost.

Then you submit the deal to your actual lenders, and the actual approval comes back at a different rate, with stipulations the buyer didn’t see, structured differently than the calculator promised. Now your F&I manager is on the phone re-selling a deal the buyer already mentally closed — at worse terms than they were quoted.

What it costs you: Buyers walk. The ones who don’t walk negotiate harder because they feel bait-and-switched. Your close rate on “online” deals tracks below your in-store rate, and you blame the leads.

What it should do: Run a real multi-lender waterfall in the buyer’s browser session. Return real approvals from real lenders with real stipulations. Let the buyer pick a real funded offer before they leave the page.

2. Stipulations get emailed after the buyer has moved on

Lenders attach conditions to approvals — proof of income, proof of insurance, references. In a traditional deal, your F&I manager clears all of that at the desk while the buyer is still in the building. Online, almost every tool punts those requests to email after the session ends.

That email arrives in an inbox where the buyer is already shopping the next dealership. It reads as friction. Most of them don’t reply.

What it costs you: Approved deals that never fund. You’ve already paid the marketing dollar to get the buyer there, the lender approved them, and you lose the deal to inbox abandonment.

What it should do: Clear stipulations during the session, in the same flow. The deal is funded before the buyer closes the tab.

3. Your online F&I PVR is a fraction of your in-store PVR

Two patterns here, both bad. Either the tool skips F&I entirely and forces the buyer back to your desk to re-buy products they thought they were done with — or it shows a generic product menu with no eligibility logic, pitching VSC plans the vehicle doesn’t qualify for and GAP that doesn’t match the financing structure.

What it costs you: PVR on online deals collapses. Your aftermarket revenue per unit on the online channel is a fraction of in-store, and your F&I team starts treating online deals as a tax. The number that should match or beat in-store benchmarks doesn’t, and you assume “online buyers don’t buy F&I” — when really, the menu was wrong.

What it should do: Surface only the products the deal is actually eligible for, given vehicle, mileage, term, and lender. Dealer-controlled pricing. Disclosure language aligned with FTC guidance.

4. The tax number at quote doesn’t match the tax number at contract

The buyer lives in a different city than your store. Maybe a different state. Sales tax on a vehicle isn’t a flat rate — it depends on the buyer’s address, state reciprocity rules, what’s taxable in the base (trade-in credit, doc fee, OEM rebates), and what’s exempt for the vehicle type.

Most checkouts use one rate. Yours. The buyer sees a number at quote that doesn’t match the number on the contract. You either eat the difference, or you call the buyer and try to explain it.

What it costs you: Either margin (you eat it) or the deal (the buyer feels jerked around). And it gets worse the further the buyer is from your store — which is exactly the buyer “online” was supposed to help you reach.

What it should do: Pull current tax tables for the buyer’s exact jurisdiction the moment they enter their address. The number at quote is the number on the contract.

5. Out-of-state buyers still need a clerk and a stack of paper

This is where most “online” platforms quietly hand the deal back to you.

Anyone can take an order on a website. Far fewer can put a license plate on a vehicle delivered to a buyer 2,000 miles away without one of your title clerks driving paperwork to a DMV office. Every state has its own document set, signature requirements, lien-perfection rules, inspection requirements, and registration windows. A motorcycle, a UTV, an LSV, a Class A motorhome, and a passenger car can each have different paths in the same state.

Encoding all of that across all 50 states — and executing it remotely without your store touching paper — is a multi-year build. Most platforms didn’t build it.

What it costs you: Your “online” channel only really works for buyers in your home state. Out-of-state buyers — exactly the incremental volume online infrastructure is supposed to unlock — get bottlenecked at your back office, your title clerk’s bandwidth, and FedEx.

What it should do: File the right forms with the right agencies in the right sequence. Surface a single status to you. Produce an issued plate to the buyer’s door without anyone at your store lifting paper.

6. A signed PDF is not a funded contract

Vehicle deals require signatures that the lender will fund against and the state will record against. The retail-installment contract in California isn’t the same form as the one in Texas. Lenders fund against their accepted templates — typeface, field placement, disclosure language. Drift in any of that delays funding or kills the deal. Many documents also require you to countersign in a specific order, with audit trail.

Most digital-retail tools deliver a flat-PDF e-sign experience. Fine for a deposit form, not enough for a contract.

What it costs you: Funding delays. Re-signs. Deals that fall apart in the week after the buyer left. Your back office spending hours per deal chasing missing signatures and re-papering contracts that didn’t match lender templates.

What it should do: Generate the document set per deal, in the lender-accepted format, sign it in the required order, and store it with a verifiable audit trail.

Real online sales runs the back office, not just the front end

A platform that delivers the buyer view of online checkout without delivering the dealer view is shifting the work, not removing it. The buyer experience may look online. The operating reality — back-office labor that doesn’t scale — is the same one your store has run for years.

A checkout-to-keys platform is a different category. Every step above runs inside the system, configured per state, per vehicle type, per financing structure. Your role is oversight and approval, not data entry. A deal jacket forms in real time as the buyer works through the flow, with every artifact attached: credit app, lender response, F&I selections, tax calc, document set, signed copies, identity verification, fraud signals, payment confirmation, title and registration paperwork.

That’s the bar. Anything short of it is online lead generation in better packaging — including the “Buy Now” button on the marketplace listing you’re paying to be on.

Five questions that expose whether your platform is real

Marketing decks won’t tell you where a tool breaks. These five will.

- Which states are you live in for full title-and-plate fulfillment, and what’s your latency from sale to issued plate by state? Vague answers mean it isn’t built.

- Show me your average F&I attach rate and PVR on online deals, by vertical. If it’s materially below in-store, the menu logic is wrong.

- Walk me through what happens to a deal where the lender attaches three stipulations. If the answer involves email after the session, count that as a leakage point.

- Demo a deal where the buyer’s address is in a different state from the dealership. Watch the tax calc, the document set, and the title flow.

- Show me a deal jacket from a closed deal three months ago. All artifacts attached, audit trail intact, clean status — or not.

A platform that can answer all five crisply is in a different category than one that can’t. The difference is what your back office actually has to do for the next 1,000 online deals.

Find out where your stack is leaking before your next 100 deals do

If you’re running a digital-retail tool today — or paying for “Buy Now” placements on the marketplaces — and you want to know where the deal is actually breaking, we’ll walk the six failure points above against your current setup and show you where the back-office work is still landing on humans. No demo pitch, just the audit.

Frequently asked questions

Not in the operating sense. Digital retail extends the in-store deal online — the buyer self-serves the easy pieces, and the back-office work stays at your desk. Real online vehicle sales runs every step end-to-end inside the system, including the labor that doesn’t scale (titling, registration, tax across jurisdictions, lender-accepted signing). Different category, different infrastructure.

No. Those buttons capture a buyer’s intent and route them to the dealer’s CRM. From there it’s the same workflow as a phone lead — a salesperson calls, an F&I manager builds the deal, a title clerk runs the paperwork. The “Buy Now” framing is marketing-side; the operating reality is lead capture. Buyers eventually figure that out and trust the channel less.

Titling and registration across state lines. Anyone can take an order; far fewer can put a plate on a vehicle delivered to a buyer in another state without a clerk driving paperwork to a DMV. It’s the step that exposes whether the platform is actually built or whether it’s a front end with manual back-office labor underneath.

They exist, and they shop differently. They tend to arrive after-hours, from outside the dealership’s local market, and with a willingness to compare across more dealers in a single session. The buyers who can’t be reached through the in-store deal — out-of-state, late-night, time-constrained — are the incremental volume online infrastructure unlocks.

Ask one question: what % of deals tagged “online” close without a salesperson, F&I manager, or title clerk touching the deal? If the answer is “all of them” — it’s real. If the answer is “almost none of them” or there’s hedging, it’s online lead generation, not online sales. The CRM and DMS will give the clean number in an afternoon.